Credit Score Factors and Tips

| Factor | % of Score | What It Means | How to Improve |

|---|---|---|---|

| Payment History | 35% | Paying bills on time | Set autopay, use reminders, pay promptly |

| Amounts Owed (Utilization) | 30% | Percentage of credit used | Keep balances low, pay down debt |

| Length of Credit History | 15% | Age and history of accounts | Keep old accounts open, limit new |

| Credit Mix | 10% | Variety of credit types | Add variety when needed |

| New Credit | 10% | Recent credit applications | Apply only when necessary |

The 5 Factors That Affect Your Credit Score (And How to Improve Each)

Understanding your credit score—and how to improve it—starts withknowing the five key components thatmake up this critical number. Here’s what influences your credit score most, along with practical tips to help you boost each factor.

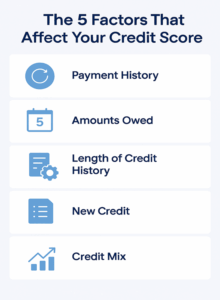

1. Payment History (35%)

What It Means:

Your history of on-time payments is the most significant factor affecting your credit score. Missed or late payments, collections, foreclosures, and bankruptcies can all lower your score.

How to Improve:

- Pay all bills by their due dates—set reminders or use autopay.

- If you’ve missed a payment, bring the accountcurrent as soon as possible.

- Contact creditors if you’re struggling; some may consider removing a reported late payment if it’s a one-time issue.

- The impact of old late payments lessens over time, especially as you build a stronger on-time record.

2. Amounts Owed / Credit Utilization (30%)

What It Means:

This factor considers how much total debt you owe—including the percentage of your available revolving credit that you’re using (your “credit utilization ratio”). Using too much of your available credit can signal higher risk.

How to Improve:

- Maintain credit card balances significantly below your credit limits—experts recommend staying below 30%, with top scores often under 10%.

- Makemultiple payments each month to reduce reported balances.

- Pay down high-balance cards first for a quickutilization improvement.

- Avoid closing unused cards, as this can reduce your overall available credit.

3. Length of Credit History (15%)

What It Means:

The longer you’ve responsibly used credit, the better.This looks at the age of your oldest and newest accounts,plus the average age of all accounts.

How to Improve:

- Keep older accounts open, even if you don’t use them often.

- Avoid openingmany new accountsin a shorttime, as thislowers your average account age.

- Start building credit early, even with a starter credit card or small loan.

4. Credit Mix (10%)

What It Means:

Lenderslook for your ability to handle various types of credit—like credit cards, mortgages, auto loans, and student loans. A healthy mix is beneficial, but you don’t need to have them all.

How to Improve:

- If youonly have one type of credit, consider diversifying when itfits your financial goals—such as adding an installment loan or credit card.

- Don’t open unnecessary accounts just for variety; only take on new credit youactually need.

5. New Credit (10%)

What It Means:

Applying for several new credit accounts in a short timeframe can lower your score, as each application triggers a “hard inquiry.”This may suggest you’re taking on new debt, which isrisky for lenders.

How to Improve:

- Apply for new credit only when necessary.

- When rate shopping (for a loan or mortgage), keep applications within a short period (usually 14–45 days); these inquiries are counted as one.

- Regularly check yourown credit score or report; these “soft inquiries” do not affect your score.

Quick Take: What Are the Main Factors That Affect Your Credit Score?

Your credit score is determined by five essential factors: payment history, credit utilization, length of credit history, credit mix, and new credit inquiries.

Improve your score by paying bills on time, keeping balances low, maintaining older accounts, diversifying your credit types thoughtfully, and only applying for new credit when needed. Every positive step helps you build a stronger financial future.

Frequently Asked Questions: Improving Your Credit Score Quickly

Q1. How fast can you improve your own credit score?

You should see noticeable improvements within a month by paying down high balances and catching up on any late accounts.

- If your negative history is recent or short-term, addressing these issues promptly can boost your score relatively fast.

- Maintaining consistent on-time payments afterward is key to sustaining progress.

Q2. Will checking my own credit hurt my credit score?

No, checking your own credit score or report is a “soft inquiry” and that does not impact your credit rating.

- You can monitor your credit as often as you’d like without any negative effect.

- This is different from “hard inquiries” that occur when the lenders check your credit for new credit applications, which can cause a small, temporary dip.

Q3. Is it better to pay off my credit card in full?

Lowering your available credit can lead to a higher credit utilization ratio, which may negatively impact your credit score.

- Avoid carrying high balances or only making minimum payments.

- This habit shows lenders you manage credit responsibly.

Q4. Does closing old accounts help or hurt?

Closing old accounts usually hurts your credit score more than it helps.

- It lowers your average age of accounts, which negatively affects your credit history length.

- It lowers your total available credit, which can raise your credit utilization ratio.

- Keeping older, positive accounts open supports a stronger credit profile.

Q5. What’s the best step to improve credit fast?

Focus on paying all bills on time and consistently reducing your revolving credit balances.

- On-time payment history is thebiggest driver of credit scores.

- Lower credit card balances improve your credit utilization ratio, often yielding quick improvements.

- Try to limithow often you apply for new credit accounts, especially within a short timeframe, asit can impact your credit score.

Have more questions? Drop them below and we’ll help you strengthen your credit profile!

Recommended Reading

Round Up Apps That Help You Save Automatically Looking for an effortless way to grow your savings? Round-up savings apps automatically help you save spare change from everyday purchases—making financial progress simple, even if you’re not a natural saver. If you’re searching for the best automatic savings apps, here’s an up-to-date comparison of how popular picks like Acorns, Chime, […]

How to Choose the Right Credit Card

How to Choose a Credit Card for Your Financial Goals How to Choose the Right Credit Card. Choosing the right credit card can be a powerful step toward reaching your money goals—whether that means earning travel rewards, maximizing cash back, or building your credit. This guide walks you through exactly how to choose a credit […]

How to Repair Your Credit Fast

How to Repair Your Credit Fast: A Step-by-Step DIY Guide Whether you’re looking to qualify for a new loan or just want a clean financial slate, you CAN repair your credit yourself—often faster than you think. This step-by-step guide gives you the actionable tools and proven strategies you need to boost your score, correct mistakes, […]

What Is a Good Credit Score? Ranges for 2024 and What They Mean Knowing what counts as your good credit score in 2024 is key if you’re aiming to get approved for loans, access lower interest rates, or strengthen your overall financial well-being. In this guide, we’ll explore the current credit score ranges, what they […]

Final Thoughts

Improving your credit score is achievable when you focus on these five essential areas. Build good payment habits, keep balances low, maintain a healthy credit mix and account age, and apply for credit only when needed. Tracking your progress helps keep you motivated on the journey to a stronger credit profile.