Methods for Legally Removing Collections from Your Credit Report

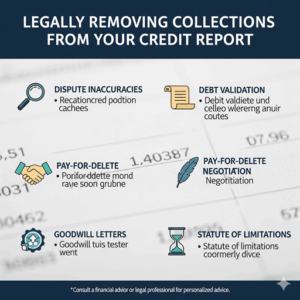

| Step/Method | Action | Legal Status and Outcome |

|---|---|---|

| Dispute Errors | File disputes with documentation | Removal if inaccurate |

| Debt Validation | Request written proof from collectors | Removal if debt is unproven |

| Pay-for-Delete | Negotiate removal in exchange for payment | Legal if agreed on in writing |

| Wait for Aging Off | Collections drop off after 7 years | Automatic and legally mandated |

How to Remove Collections from Your Credit Report (Legally)

If you’ve discovered a collection account dragging down your credit, it’s important to know how to remove collections from your credit report—and do it legally. Whether the collection is an error or a legitimate debt, there are steps you can take to clean up your credit profile and work toward a stronger score. This guide covers the safest, most effective strategies you can use to legally remove collections from your credit report.

Quick Take: Legally Remove Collections from Your Credit Report

The best ways to remove collections from your credit report legally include disputing inaccuracies, requesting debt validation, negotiating “pay-for-delete” agreements, or waiting for collections to age off. Every step must follow credit laws for safe, lasting results.

Step-by-Step: How to Remove Collections from Credit Report (Legally)

1. Review Your Credit Reports Thoroughly

-

Get your reports from all three credit bureaus (Experian, Equifax, and TransUnion).

-

Look for all collection accounts, noting amounts, dates, and the agency involved.

-

Double-check for errors, such as duplicates, debts that aren’t yours, or accounts past the seven-year reporting limit.

2. Dispute Inaccurate Collections

One of the quickest ways to legally remove collections from your credit report is to file a dispute if the information is wrong.

-

Provide documents that prove your case (payment records, account statements, or identity verification).

-

File your dispute online or by mail with each bureau reporting the error.

-

If the bureau can’t verify the collection or finds it inaccurate, it must be deleted.

3. Request Debt Validation

You have the legal right to request a review of your debt validation from any collection agency.

-

Write to the collector within 30 days of their first contact, asking for written proof of the debt.

-

If the agency can’t validate the debt (for example, wrong amount or identity), they must remove it from your credit report.

4. Negotiate “Pay-for-Delete”

Sometimes, you can negotiate directly with the collector—offering payment in exchange for removal.

-

Ask for a “pay-for-delete” agreement in writing.

-

If the agency agrees, pay the negotiated amount and keep copies of all correspondence.

-

Remember: Not all collectors will honor this, but it’s a legal and sometimes effective option to remove collections from your credit report.

5. Monitor and Wait for Collections to Age Off

-

Collections must be removed from your credit report, but only after seven years from the date of first delinquency, as required by law.

-

After paying or resolving the debt, track your reports to ensure the status updates to “paid” (if not deleted).

-

If a collection remains longer than legally allowed, dispute it for removal.

Frequently Asked Questions: Collections and Your Credit Report

Q1. Can paying off a collection remove it from my report?

Not automatically.

-

-

When you pay a collection, the status changes to “paid,” but the account will remain on your credit report until it ages off—usually after 7 years from the original delinquency date.

-

The exception: If you negotiate a “pay for delete” and the collection agency agrees in writing, they may remove it after payment, but this isn’t guaranteed.

-

Q2. What if the collection isn’t mine?

Take action by disputing the entry with each credit bureau.

-

-

Request debt validation from the collection agency—ask them to provide proof that you owe the debt.

-

If they cannot verify the debt or if it’s clearly not yours, the collection must be removed from your credit report.

-

Disputes can be submitted online, by mail, or by phone, but keep copies of all your communications and responses.

-

Q3. Is “pay for delete” legal?

Yes, but it’s not guaranteed.

-

-

Collection agencies are allowed to remove collection accounts in exchange for payment, but they are not required by law to do so.

-

If you negotiate a “pay for delete,” always get the agreement in writing before making any payment.

-

Even with a written promise, some agencies may not follow through, so follow up with both the agency and the credit bureaus after payment.

-

Q4. Will removing a collection improve my score?

Yes, particularly if the collection is unpaid.

-

-

The positive impact is typically greater when a collection is deleted outright, especially if it was unpaid.

-

If marked as “paid,” the collection is less damaging than “unpaid,” and its impact on your score lessens over time.

-

Removing collections can improve your chances for loan approvals and may result in higher scores, depending on your credit history overall.

-

Q5. How can I protect my credit during this process?

Stay proactive and maintain good credit habits:

-

-

Always pay your other accounts (loans, credit cards, utilities) on time.

-

Keep credit card balances low relative to your limits.

-

Regularly monitor your credit reports for errors, updates to the collection account, or new collections.

-

Respond to any notices from debt collectors right away and keep documentation of all communications.

-

If you notice any inaccuracies, dispute them promptly with the credit bureaus.

-

Have more questions? Drop them below and we’ll help you navigate your path to better credit!

Recommended Reading

Round Up Apps That Help You Save Automatically Looking for an effortless way to grow your savings? Round-up savings apps automatically help you save spare change from everyday purchases—making financial progress simple, even if you’re not a natural saver. If you’re searching for the best automatic savings apps, here’s an up-to-date comparison of how popular picks like Acorns, Chime, […]

How to Choose the Right Credit Card

How to Choose a Credit Card for Your Financial Goals How to Choose the Right Credit Card. Choosing the right credit card can be a powerful step toward reaching your money goals—whether that means earning travel rewards, maximizing cash back, or building your credit. This guide walks you through exactly how to choose a credit […]

How to Repair Your Credit Fast

How to Repair Your Credit Fast: A Step-by-Step DIY Guide Whether you’re looking to qualify for a new loan or just want a clean financial slate, you CAN repair your credit yourself—often faster than you think. This step-by-step guide gives you the actionable tools and proven strategies you need to boost your score, correct mistakes, […]

What Is a Good Credit Score? Ranges for 2024 and What They Mean Knowing what counts as your good credit score in 2024 is key if you’re aiming to get approved for loans, access lower interest rates, or strengthen your overall financial well-being. In this guide, we’ll explore the current credit score ranges, what they […]

Final Thoughts

Removing collections from your credit report is possible through accurate disputes, validation, negotiation, and, in some cases, patience. Knowing your rights and staying organized will give you the best chance for a lasting, healthy credit profile.